Venmo’s New Cash Back Program Looks Good. Until You Read the Fine Print

Venmo just launched a rewards program that promises up to 5 percent cash back. Sounds amazing, right? But there’s a catch. Actually, several catches.

PayPal rolled out Venmo Stash this week for debit card users. The program scales rewards based on how deeply you commit to Venmo’s ecosystem. More engagement equals more cash back. Yet the details reveal why this might disappoint most users.

You Can’t Spend Anywhere

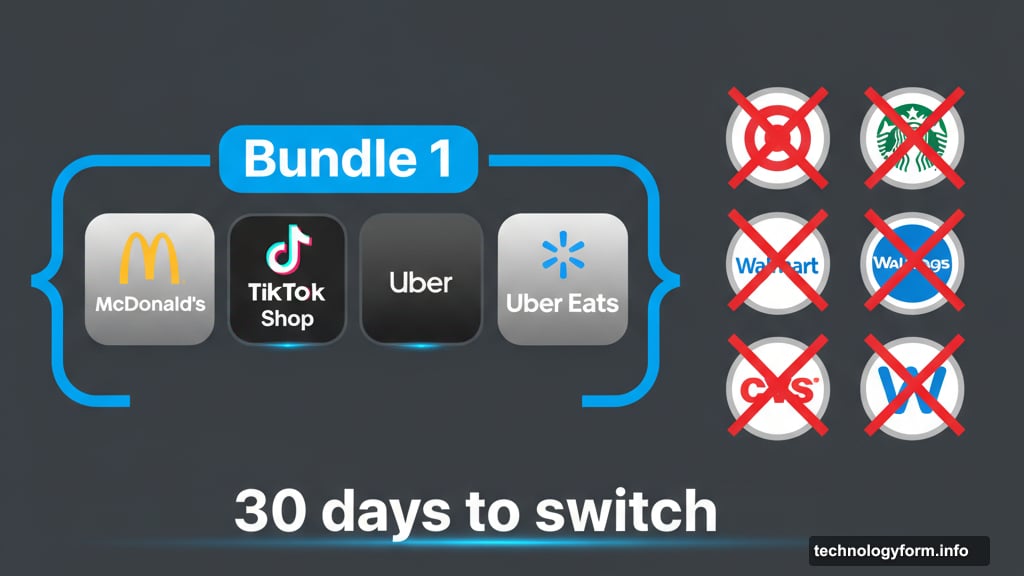

Here’s the big problem. Cash back only applies at specific brand bundles.

Venmo groups merchants into curated collections. One bundle might include McDonald’s, TikTok Shop, Uber and Uber Eats. Another features Amazon, DoorDash, Domino’s and Walgreens. Users pick one bundle and can switch every 30 days.

So if you spend $500 at Target this month but Target isn’t in your chosen bundle? Zero rewards. That $200 grocery run at Kroger? Nothing unless Kroger made the cut.

This dramatically limits where rewards actually apply. Most people spend money at dozens of merchants monthly. But Venmo restricts rewards to maybe four or five brands at once.

The Reward Tiers Demand Commitment

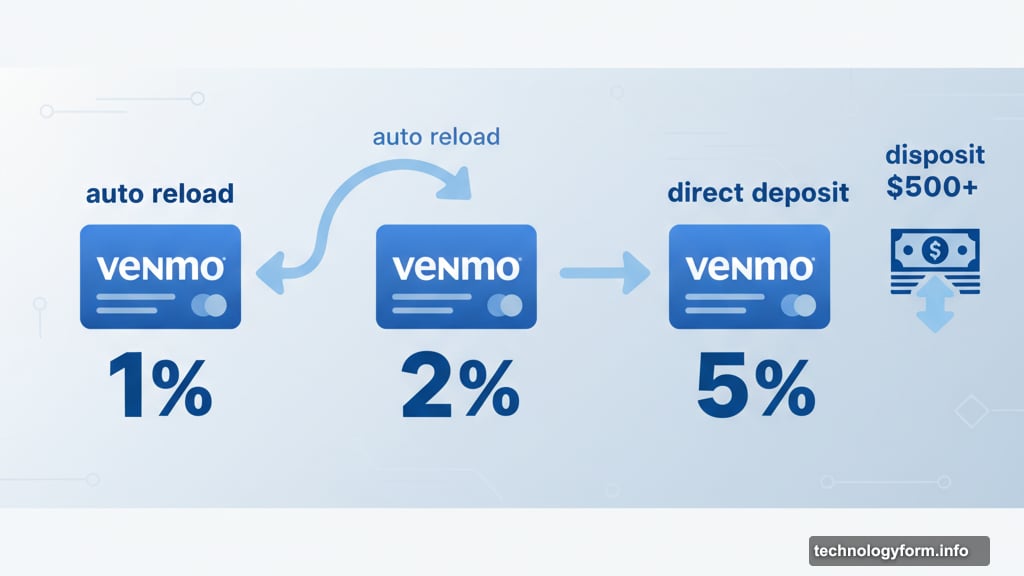

Cash back starts low and requires jumping through hoops to increase.

The base tier offers 1 percent back when you spend at bundle brands. That’s already below what many credit cards provide everywhere. Plus, you’ll bump up against merchant restrictions immediately.

Hitting 2 percent requires enabling auto reload. This feature automatically adds money to your Venmo balance when it drops below a threshold. So you’re keeping funds locked in Venmo instead of your bank account earning interest.

The top 5 percent tier demands even more. You need monthly direct deposits of at least $500 into Venmo. That means routing your paycheck through Venmo instead of a traditional bank. For many people, that’s a nonstarter.

Monthly Caps Kill Long-Term Value

Venmo buries another restriction in the fine print. There’s a monthly reward cap.

The exact cap amount only appears during enrollment. Once you hit it, rewards stop completely until next month. So even if you max out the 5 percent tier and spend heavily at bundle merchants, you’ll eventually earn nothing.

Traditional credit cards don’t impose these arbitrary monthly limits. You earn rewards on every qualifying purchase, period. Venmo’s approach means your effective cash back rate drops as spending increases.

Moreover, switching bundles takes 30 days. If your spending patterns change mid-month, you’re stuck earning zero rewards at newly relevant merchants.

PayPal Wants You All In

This program fits PayPal’s recent push to become your financial hub.

Earlier this year, PayPal offered free Perplexity Pro subscriptions to users. They also provided early access to Comet, an AI-powered browser. These perks share one goal: keep you engaged with PayPal products.

Venmo Stash follows the same playbook. It dangles attractive rewards but requires committing your financial life to Venmo. Direct deposits, auto reloads, specific spending patterns. Each requirement deepens your reliance on their platform.

That’s fine if Venmo genuinely serves your needs. But most people use multiple financial tools for good reasons. Banks offer better interest rates. Credit cards provide superior fraud protection. Specialized apps handle budgeting or investing more effectively.

Better Options Exist

Traditional cash back credit cards beat Venmo Stash for most users.

Many cards offer 2 percent back on everything with no restrictions. No bundle limitations. No monthly caps. No requirement to route your paycheck through the card company. Just straightforward rewards on all purchases.

Plus, credit cards provide robust fraud protection that debit cards can’t match. If someone steals your credit card number, you’re not liable for fraudulent charges. With debit cards, thieves access your actual money. Recovery takes longer and isn’t guaranteed.

Even PayPal’s own credit card offers better terms than Venmo Stash. It provides 2 percent cash back on all purchases without the bundle restrictions or monthly caps.

The Restrictions Outweigh the Rewards

Venmo markets 5 percent cash back aggressively. But reaching that tier requires sacrifices most people won’t make.

You need direct deposits of $500 monthly. You must keep funds in Venmo via auto reload. You can only earn rewards at a handful of merchants. Monthly caps limit total earnings. And switching bundles takes 30 days.

Stack those restrictions together and the effective cash back rate drops dramatically. Unless your spending perfectly aligns with available bundles, you’ll earn far less than 5 percent. For many users, the real rate might approach 1 percent or less.

That’s not competitive. It’s barely worth the hassle of managing another payment method.

PayPal Needs to Do Better

This program feels half-baked. It dangles attractive numbers but delivers far less value than advertised.

If PayPal wants to compete seriously in rewards programs, they need to eliminate artificial restrictions. Remove bundle limitations. Ditch monthly caps. Let users earn consistent rewards everywhere, just like credit cards do.

Until then, Venmo Stash serves PayPal’s interests more than users. It locks customers into Venmo’s ecosystem without providing compelling value in return. Most people will earn more using a straightforward 2 percent cash back credit card instead.

Skip this one. Your wallet will thank you.