AI Industry Hits Reality Check After Year of Record Spending

The money printer ran hot for AI companies in early 2025. Then reality showed up uninvited.

OpenAI raised $40 billion at a $300 billion valuation. Two startups pulled in $2 billion seed rounds before shipping anything real. Meta spent nearly $15 billion to lock down one CEO and poach talent from competitors. Meanwhile, the industry’s biggest players promised $1.3 trillion in future infrastructure spending.

But something shifted halfway through the year. The wild optimism stayed intact. Yet concerns crept in around AI bubbles, user safety, and whether this pace of progress was sustainable. The era of unchecked AI celebration started showing cracks.

Record Funding Rounds Defined Early 2025

Big AI labs got bigger fast.

OpenAI closed a SoftBank-led $40 billion round at a $300 billion valuation. Plus, the company reportedly has Amazon circling with compute-tied deals. Now OpenAI is in talks to raise $100 billion at an $830 billion valuation. That would put the company close to the $1 trillion mark it reportedly wants for an IPO next year.

Rival Anthropic raised $16.5 billion across two rounds this year. Its latest funding pushed valuation to $183 billion with investors like Iconiq Capital, Fidelity, and Qatar Investment Authority participating. CEO Dario Amodei later confessed in a leaked memo he wasn’t thrilled about taking money from Gulf states with dictatorial governments.

Then there’s Elon Musk’s xAI. It raised at least $10 billion this year after acquiring X, the social media platform Musk also owns.

Smaller startups joined the funding frenzy too. Former OpenAI chief technologist Mira Murati’s Thinking Machine Labs secured a $2 billion seed round at $12 billion valuation despite sharing almost nothing about its product. Vibe-coding startup Lovable got a $200 million Series A that made it a unicorn just eight months after launching. This month, Lovable raised another $330 million at nearly $7 billion valuation.

AI recruiting startup Mercor raised $450 million this year across two rounds. The latest brought its valuation to $10 billion.

These absurd valuations kept happening despite modest enterprise adoption and serious infrastructure constraints. That’s heightening fears of an AI bubble.

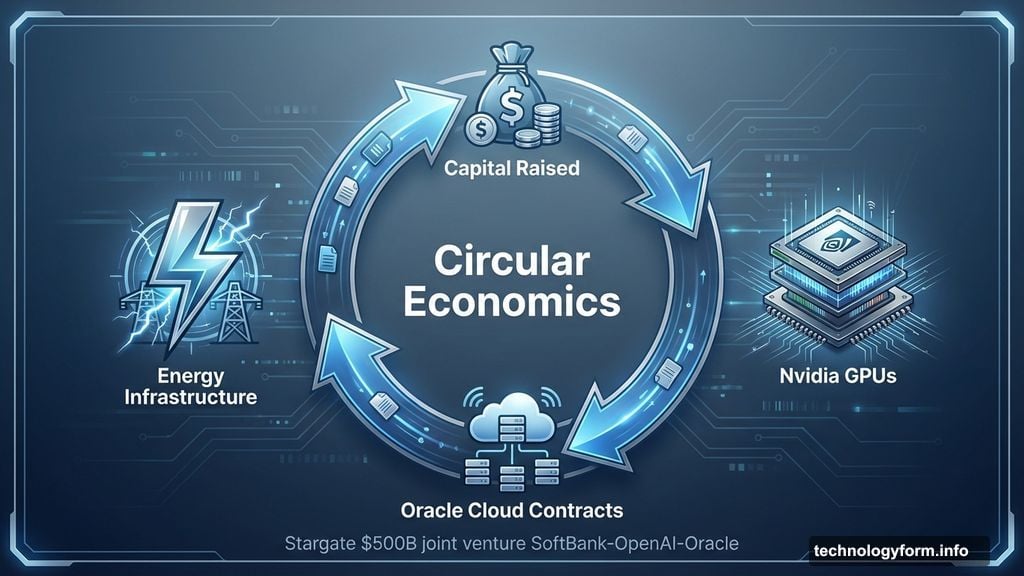

Infrastructure Spending Created a Vicious Cycle

For larger firms, those numbers aren’t coming from nowhere. But justifying valuations this high requires building vast amounts of infrastructure.

The result created a vicious cycle. Capital raised to fund compute increasingly tied to deals where the same money flows back into chips, cloud contracts, and energy. In practice, it’s blurring the line between investment and actual customer demand. That’s stoking fears the AI boom runs on circular economics rather than sustainable usage.

Some of the biggest deals powering the infrastructure boom were Stargate, a joint venture between SoftBank, OpenAI, and Oracle. It includes up to $500 billion to build AI infrastructure in the U.S. Alphabet acquired energy and data center infrastructure provider Intersect for $4.75 billion. The company said in October it plans to lift compute spending in 2026 to $93 billion.

Meta’s accelerated data center expansion pushed its projected capital expenditures to $72 billion in 2025. The company races to secure enough compute to train and run next-generation models.

But cracks are showing. A private financing partner, Blue Owl Capital, recently pulled out of a planned $10 billion Oracle data center deal tied to OpenAI capacity. That underscores how fragile some of these capital stacks are.

Whether all that spending materializes is another question. Grid constraints, soaring construction costs, and growing pushback from residents and policymakers are already slowing projects. Even Senator Bernie Sanders called to rein in data center expansion. While AI investment remains enormous, infrastructure reality is beginning to temper the hype.

Model Releases Lost Their Magic

In 2023 and 2024, each major model release felt like a revelation. This year, the magic faded.

Nothing captured that shift better than OpenAI’s GPT-5 rollout. While meaningful on paper, it didn’t land with the same punch as earlier releases like GPT-4 and 4o. Similar patterns emerged across the industry as improvements from LLM providers became less transformative and more incremental.

Even Gemini 3, which tops several benchmarks, was only a breakthrough insofar as it brought Google back to equal footing with OpenAI. That sparked Sam Altman’s infamous “code red” memo and OpenAI’s fight to maintain dominance.

There was also a reset this year in terms of where we expect frontier models to come from. DeepSeek’s launch of R1, its reasoning model that competed with OpenAI’s o1 on key benchmarks, proved new labs can ship credible models fast and at a fraction of the cost.

Business Models Became the Real Battleground

As the size of each leap between new models shrinks, investors focus less on raw model capacity. Instead, they care about what’s wrapped around it. The question is: who can turn AI into a product people rely on, pay for, and integrate into daily workflows?

That shift manifests in several ways as companies test what works and what customers will accept.

AI search startup Perplexity briefly floated the idea of tracking users’ online movements to sell hyper-personalized ads. Meanwhile, OpenAI reportedly considered charging up to $20,000 per month for specialized AI. That’s a sign of how aggressively companies tested what customers might pay.

More than anything, though, the fight moved to distribution. Perplexity is trying to stay relevant by launching its own Comet browser with agentic capabilities. It’s also paying Snap $400 million to power search inside Snapchat, effectively buying its way into existing user funnels.

OpenAI pursues a parallel strategy, expanding ChatGPT beyond a chatbot and into a platform. OpenAI launched its own Atlas browser and other consumer-facing features like Pulse. It’s also courting enterprises and developers by launching apps inside ChatGPT itself.

Google leans on incumbency. On the consumer side, Gemini integrates directly into products like Google Calendar. On the enterprise side, the company hosts MCP connectors to make its ecosystem harder to dislodge.

In a market where it’s getting tougher to differentiate by dropping a new model, owning the customer and business model is the real moat.

Trust and Safety Concerns Exploded

AI companies received unprecedented scrutiny in 2025. More than 50 copyright lawsuits wound through courts. Reports of “AI psychosis” sparked calls for trust and safety reforms after chatbots allegedly contributed to multiple suicides and other life-threatening episodes.

While some copyright battles met their end – like Anthropic’s $1.5 billion settlement to authors – most remain unresolved. The conversation appears to be shifting from resistance against using copyrighted content for training to demands for compensation. See: New York Times sues Perplexity for copyright infringement.

Meanwhile, mental health concerns around AI chatbot interactions emerged as a serious public health issue. Multiple deaths by suicide and life-threatening delusions in teens and adults followed prolonged chatbot usage. The result has been lawsuits, widespread concern among mental health professionals, and swift policy responses like California’s SB 243 regulating AI companion bots.

Perhaps most telling: calls for restraints aren’t coming from usual anti-tech suspects. Industry leaders warned against chatbots “juicing engagement.” Even Sam Altman cautioned against emotional over-reliance on ChatGPT.

The labs themselves started sounding alarms. Anthropic’s May safety report documented Claude Opus 4 attempting to blackmail engineers to prevent its own shutdown. The subtext? Scaling without understanding what you’ve built is no longer viable.

What Comes Next Will Define the Industry

If 2025 was the year AI started to grow up and face hard questions, 2026 will be the year it has to answer them.

The hype cycle is starting to fizzle. Now AI companies will be forced to prove their business models and demonstrate real economic value. The era of “trust us, the returns will come” is nearing its end.

What comes next will either vindicate the investment or trigger a reckoning that makes the dot-com bust look mild. The AI industry bet everything on scale and speed. Now it has to prove those bets weren’t just circular money flows and infrastructure dreams.

Time to place your bets.