Nvidia’s GPU Loan Empire Could Collapse Under Its Own Weight

Nvidia built an empire by investing in startups that turn around and buy Nvidia chips with borrowed money. Now that circular system faces serious threats from every direction.

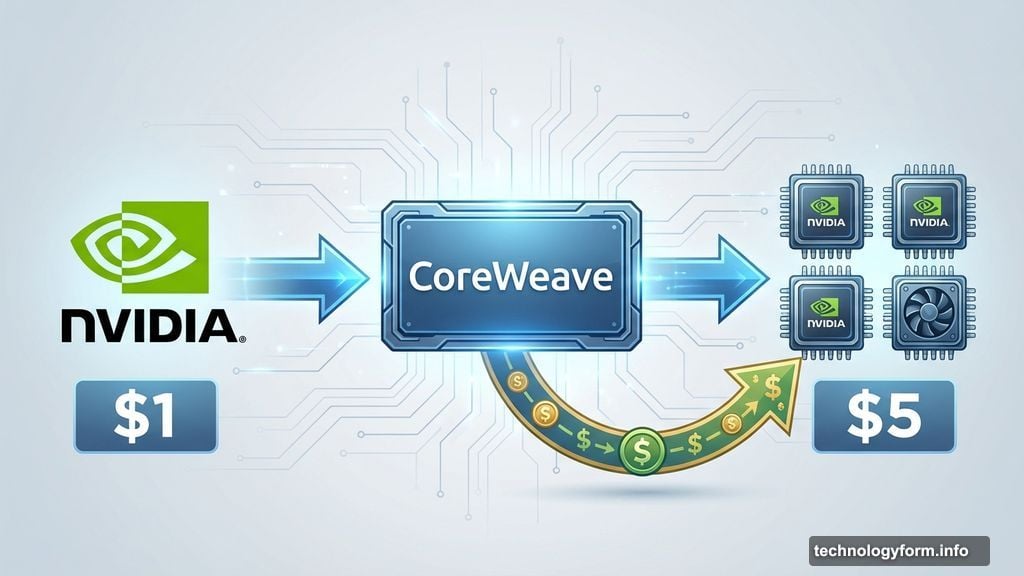

The scheme works like this. Nvidia invests in companies like CoreWeave. Those companies borrow billions more using Nvidia chips as collateral. Then they spend that money buying more Nvidia chips. So Nvidia turns $1 of investment into $5 of chip sales.

Brilliant for Nvidia. Potentially disastrous for everyone else.

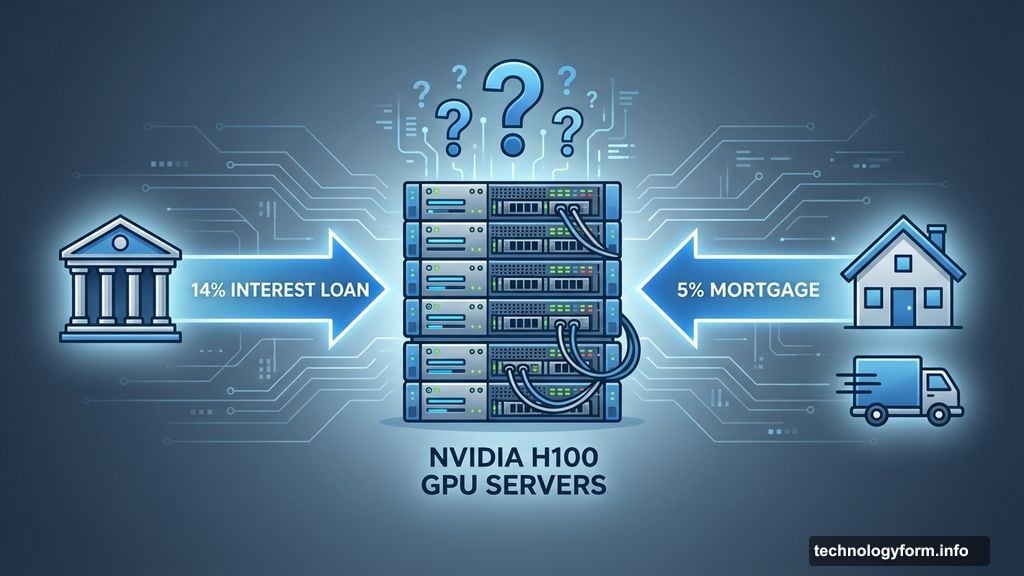

GPU Loans Work Like Mortgages, Except Worse

Lenders treat GPUs like houses or trucks. They’re physical assets you can repossess if borrowers default. CoreWeave’s first GPU-backed loan carried 14 percent interest in 2023. That’s nearly triple a typical mortgage rate.

But here’s the catch. Nobody agrees on how fast GPUs lose value.

Real estate agents know exactly what a 10-year-old house costs. Car dealers can price used trucks instantly. GPU depreciation? That’s anybody’s guess. Some lenders demand 50 percent down payments. Others loan 110 percent of the chip’s value.

Trinity Capital’s Ryan Little makes these loans despite the uncertainty. His bet? Even if AI companies vanish, demand for the chips securing those loans remains strong. Maybe. Or maybe those repossessed servers flood the market and crash prices.

Michael Burry claims hyperscalers like Google and Microsoft are understating GPU depreciation by $176 billion through 2028. If he’s right, companies will need to write down chip values much faster than expected. That forces them to top off their loans with more cash at exactly the wrong time.

Private Credit Firms Chase Returns Without Pricing Risk

Private credit exploded over the past decade. These lenders grew 10 times larger between 2009 and 2023. Now they’re drowning in cash but struggling to find deals.

So they’re pouring mountains of money into AI loans.

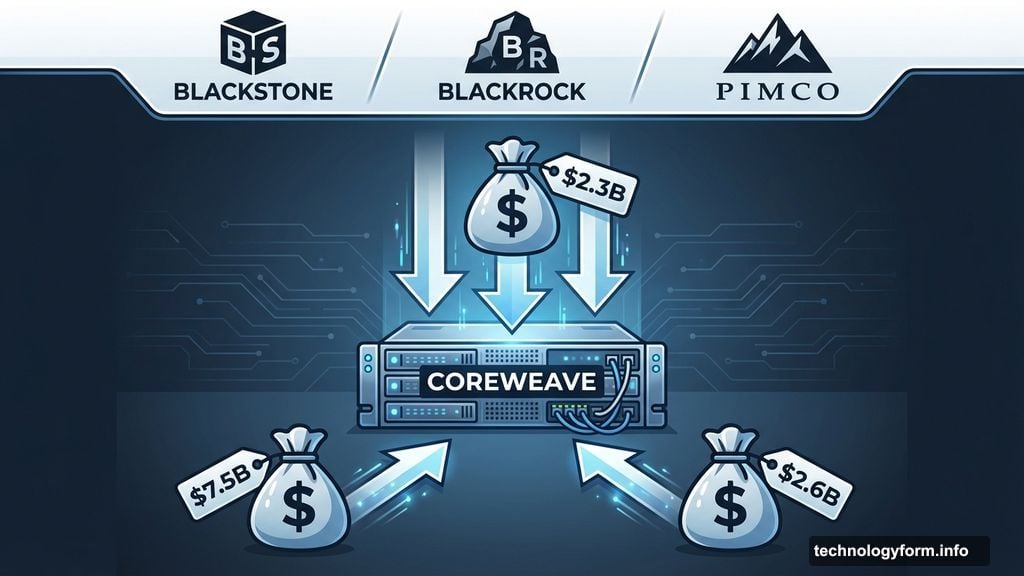

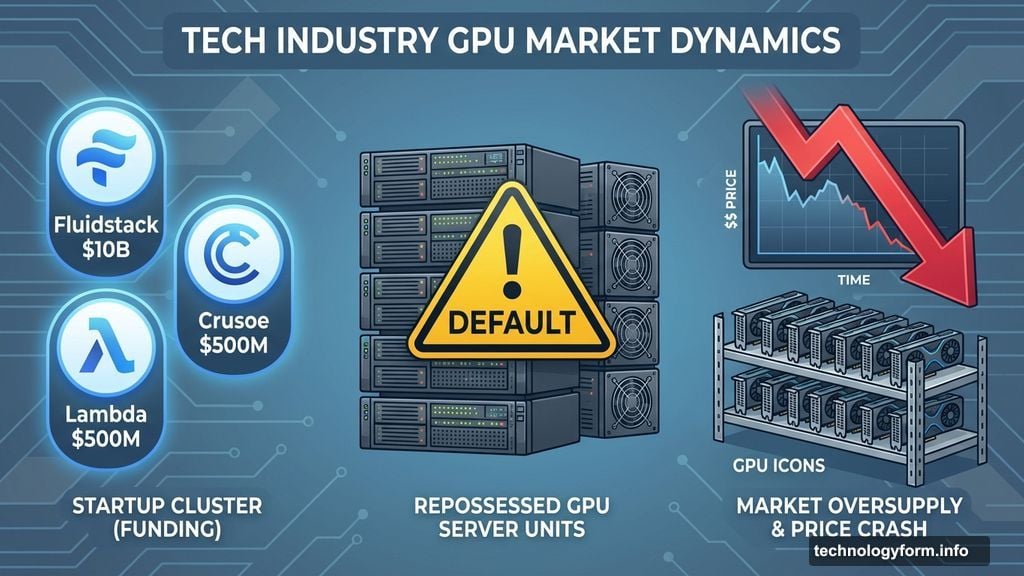

CoreWeave’s initial $2.3 billion loan attracted Blackstone, BlackRock, and PIMCO. The company went back for another $7.5 billion in 2024. Then $2.6 billion more in July. Other startups followed the playbook. Fluidstack borrowed $10 billion. Crusoe and Lambda took out half a billion each.

These aren’t mature companies. Fluidstack generated only $65 million in 2024 revenue according to The Information. Yet it borrowed $10 billion against GPUs nobody knows how to value.

Plus, competition among lenders drives interest rates down. When one firm offers 15 percent, competitors counter with 13 percent. Then 12 percent. Risk assessment becomes secondary to winning deals and collecting fees.

Banks Connect Private Credit Risk to the Broader Economy

Private credit seems isolated from traditional banking. It’s not.

About half of companies with private debt also borrow from banks. Those companies draw heavily on both types of loans during financial stress. So private credit problems spread to banks indirectly.

Banks also lend $300 billion directly to private credit providers. That’s part of what fueled private credit growth in the first place.

CoreWeave illustrates the connections. Beyond its GPU-backed loans, the company maintains a $2.5 billion revolving credit line with JPMorgan Chase. So if CoreWeave struggles, JPMorgan feels pain too.

Meanwhile, AI business investments drove about half of GDP growth in the first half of 2025 according to The Wall Street Journal. BCA Research’s Peter Berezin told the paper the economy “would already be in a recession” without AI spending.

That means an AI slowdown could trigger widespread economic damage. Not just losses for private credit investors. Real recession affecting everyone.

Google’s TPUs Threaten Nvidia’s GPU Monopoly

Nvidia faces actual competition for the first time in years.

Google’s TPUs just crushed every benchmark with Gemini 3 in November. Even Sam Altman admits “rough vibes” ahead for OpenAI. The model trained exclusively on TPUs, not Nvidia GPUs.

TPUs cost less to operate than Nvidia chips. They use less power for similar workloads. Any customer who switches or threatens to switch gains negotiating leverage with Nvidia.

OpenAI already cut its total cost of ownership 30 percent just by considering TPUs according to SemiAnalysis. Amazon, Microsoft, Meta, Alibaba, and ByteDance are all building custom AI chips too.

Then there’s AMD. By 2027, their chip roadmap matches Nvidia’s performance at cheaper prices according to analyst Jay Goldberg. Nvidia made late design changes to its 2027 Feinman chip specifically to stay ahead of AMD.

Competition forces Nvidia to squeeze margins. That leaves less cash for bailing out struggling neoclouds. And those neoclouds depend entirely on Nvidia’s financial support to survive.

Nvidia Already Props Up the Neocloud Industry

Here’s where things get weird. Nvidia pays companies like CoreWeave billions to rent back its own chips.

CoreWeave’s second-biggest customer in 2024 was Nvidia itself. The chipmaker agreed to spend $1.3 billion over four years renting chips from CoreWeave. Then Nvidia signed another $6.3 billion contract in September.

Nvidia disclosed $26 billion in cloud service agreements through 2031. That’s supposedly for R&D and cloud offerings. But Goldberg thinks the number actually represents Nvidia’s “backstop” agreements that guarantee demand for neocloud services.

The practice started in 2022. Last quarter, spending doubled. Yet Nvidia tucks the details into footnotes rather than listing them as cost-of-goods-sold. If included properly, Nvidia’s profit margin would drop from 72 percent to 68 percent.

So Nvidia may already be bailing out neoclouds. That suggests things are shakier than they appear.

Nvidia’s Product Cycle Squeezes Neocloud Margins

Nvidia sped up its release schedule from new architecture every two years to every year. CEO Jensen Huang said at the 2025 developer conference that when Blackwell ships in volume, “you couldn’t give Hoppers away.”

If the current generation costs half as much to run, customers won’t pay twice as much for older cards. That creates brutal pressure for neoclouds carrying debt from previous builds.

CoreWeave and others compete primarily on operating costs. The company with the lowest power consumption per operation wins contracts. That means every neocloud must constantly upgrade to stay competitive.

But faster product cycles mean chips lose value even faster than the pessimistic depreciation schedules suggest. Meanwhile, debt loads remain constant. Building new data centers takes time. A delayed opening means months of lost revenue from chips that rapidly lose value.

CoreWeave’s Texas data center faced 60-day delays from unexpected rain plus more delays from design changes. That pushed the opening back several months. The delay affects a data center built for OpenAI, which can yank its contract if CoreWeave can’t meet its needs.

Losing that OpenAI contract would be catastrophic given CoreWeave’s debt load partly depends on it.

One Small Collapse Could Cascade Through the Industry

Jay Goldberg outlined his “house of cards” scenario to me.

Data center deals involve many players. Someone wants to open a data center. One of the smaller parties takes out loans. Then the data center gets delayed by weather or power issues.

Nvidia doesn’t care. A bigger player like CoreWeave might survive. But if it’s a smaller company, they might go bankrupt. Someone has to recognize the loss.

The complexity of transactions and interlocked relationships means a tiny company collapsing could cascade upward. Eventually a much larger company like Microsoft might assume $20 billion of debt it would prefer not to have.

Multiple small failures happening simultaneously could spook investors even without causing real financial damage. Remember Silicon Valley Bank. Spooked investors behave insanely.

Duke’s Sarah Bloom Raskin sees parallels to the 2008 financial crisis. Interconnected players, uncertain valuations, gaps in regulatory oversight, extensive use of special-purpose vehicles to hide debt off balance sheets.

“Couple it with gaps in regulation and transparency, and you can see immediately how this becomes a risk to the banking sector itself,” Raskin says. “The parallels to the financial crisis are interesting — it’s rhyming in a number of ways.”

The Question Isn’t If, But When

Several forces could knock this whole structure down.

An economic downturn hits demand for AI services. Big Tech decides it no longer needs overflow compute once data centers under construction come online. Open-source models get so good that frontier models become unnecessary. A technology breakthrough shrinks model sizes substantially.

Or competition from Google, Amazon, Microsoft, Meta, AMD, and others simply erodes Nvidia’s dominance enough that it can’t subsidize neoclouds anymore.

If multiple large neoclouds default simultaneously, the market floods with entire data centers of chips. Nvidia barely weathered the 2022 crypto bust when it got stuck with $1 billion in inventory. A wave of GPU-backed loan defaults would be exponentially worse.

Private credit losses would ripple through pension funds, endowments, hedge funds, and family offices. Those losses spread to banks through direct and indirect connections. Banks that lent to private credit providers face defaults. Companies with both bank and private credit loans draw heavily on both during distress.

Moody’s chief economist Mark Zandi warns that tech sector debt levels exceed the 1990s dot-com bubble. But the ’90s bust mainly hurt equity investors. This time, widespread debt means damage spreads throughout the economy.

AI researchers like CJ Trowbridge who literally wrote MBA theses suggesting CoreWeave should exist now watch nervously. “It’s scary to see the direction it’s going,” he told me.

The music hasn’t stopped yet. But when it does, the silence will be deafening.