PayPal Wants to Become a US Bank. Trump’s Rules Make It Easier

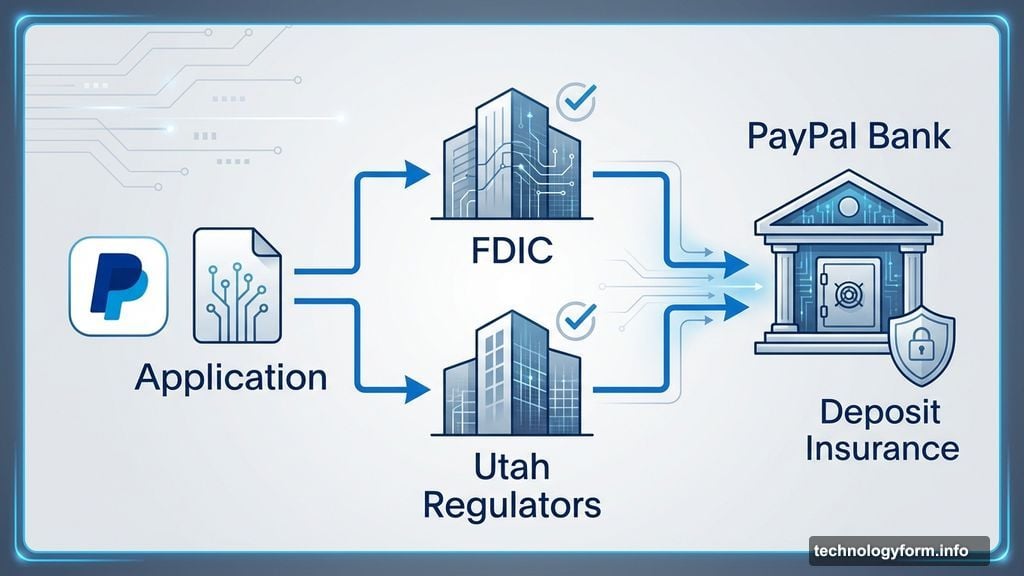

PayPal just filed paperwork to become a real bank in America. The company submitted applications to the FDIC and Utah regulators on Monday, hoping to launch PayPal Bank.

This isn’t some random expansion. PayPal already runs a bank in Luxembourg and has pumped over $30 billion in loans to 420,000 businesses worldwide. But operating as a US bank changes everything. It means direct access to federal banking infrastructure, deposit insurance, and regulatory oversight that could actually strengthen the business.

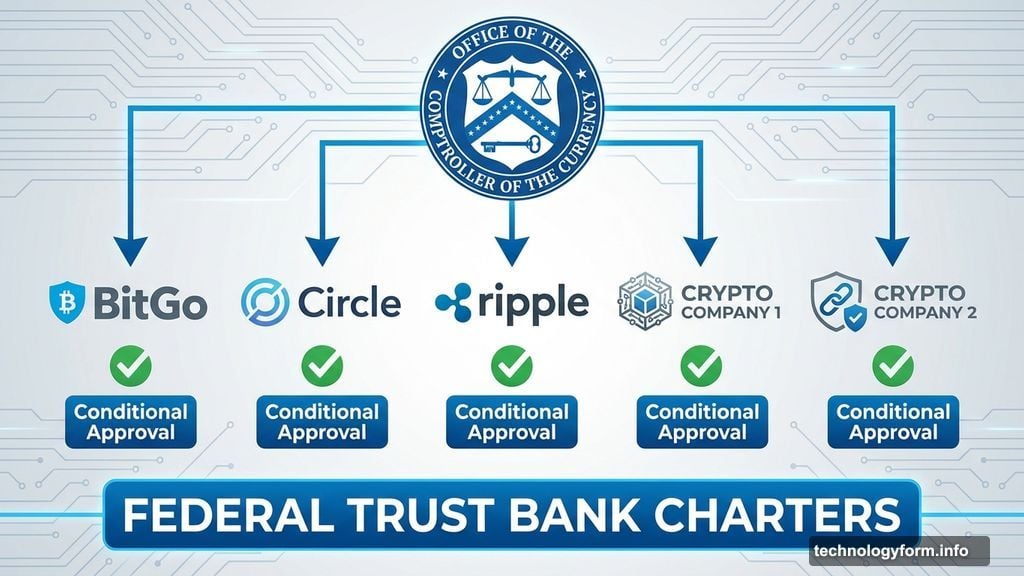

Plus, PayPal isn’t alone. Five crypto companies just got conditional approval to become federally chartered trust banks last Friday. Nissan and Sony filed applications too. Something changed in the banking approval process, and companies are racing to capitalize.

Small Business Lending Gets Priority

PayPal’s pitch centers on small business struggles. CEO Alex Chriss framed the bank application around capital access challenges that hold back growth.

“Securing capital remains a significant hurdle for small businesses striving to grow and scale,” Chriss stated in the company’s release. The subtext is clear. Traditional banks often ignore small businesses or saddle them with brutal terms. PayPal wants to position itself as the alternative.

The company plans to offer business loans and working capital directly through PayPal Bank. Given their existing track record of $30 billion deployed globally, they’ve already proven they can assess risk and move money. Banking charter just makes the infrastructure cleaner and potentially cheaper.

Moreover, PayPal plans interest-bearing savings accounts. For consumers and businesses holding PayPal balances, this creates actual value instead of dead money sitting in accounts. It’s a logical extension of their existing financial services.

Trump Administration Opens Banking Floodgates

The timing isn’t coincidental. Banking applications exploded under loosened Trump-era regulatory approaches.

Last Friday’s announcement from the Office of the Comptroller of the Currency (OCC) tells the story. BitGo, Circle, Ripple, and two other crypto firms received conditional approval for federal trust bank charters. That would’ve been nearly impossible during previous administrations’ stricter oversight.

“New entrants into the federal banking sector are good for consumers, the banking industry and the economy,” OCC comptroller Jonathan V. Gould declared. The statement signals a fundamental shift in regulatory philosophy. More competition equals better outcomes, according to this view.

However, critics worry about risk. Banking regulations exist because bank failures devastate economies. The 2008 financial crisis proved what happens when oversight weakens. So while competition sounds great, hastily approved banks could create systemic problems down the road.

Still, PayPal represents less risk than pure crypto plays. The company has operated legitimate financial services for decades. They understand compliance, fraud prevention, and customer protection. Their bank application feels more evolution than revolution.

Utah Becomes Fintech Banking Hub

PayPal chose Utah for its charter location. That’s not random either.

Utah actively courts fintech companies with favorable regulations and cooperative state banking authorities. The Utah Department of Financial Institutions (UDFI) has approved multiple fintech bank charters in recent years. Companies appreciate the state’s balance between oversight and innovation.

For PayPal, a Utah charter means operating under state and federal regulations simultaneously. The FDIC provides deposit insurance. Utah provides the legal framework. Together, they create the infrastructure PayPal needs to function as a full-service bank.

Meanwhile, Silicon Valley Bank’s collapse last year reminded everyone that even established banks can fail. Regulators supposedly learned lessons from that debacle. Whether those lessons stick remains unclear, especially with regulatory enthusiasm for approving new entrants.

What Customers Actually Get

Banking status changes what PayPal can offer. Currently, they partner with banks to provide services. Becoming a bank eliminates the middleman.

First, direct lending becomes cheaper and faster. No intermediary bank means PayPal keeps more profit and can potentially offer better rates. Small businesses might actually benefit from improved terms and quicker approvals.

Second, savings accounts gain FDIC insurance up to standard limits. That protection matters when you’re parking real money somewhere. PayPal balances currently don’t carry the same guarantees unless specifically held in FDIC-insured accounts through partner banks.

Third, PayPal gains access to Federal Reserve systems directly. That reduces transaction costs and speeds up money movement. For a payments company, direct Fed access is hugely valuable.

But customers might not notice much difference initially. PayPal will still look like PayPal. The backend infrastructure changes create opportunities for future products and potentially better pricing. The immediate user experience probably stays similar.

Banking Applications Keep Coming

PayPal joins a growing list of non-traditional companies pursuing bank charters. Nissan filed to create a bank focused on auto financing. Sony wants banking infrastructure for its entertainment and electronics ecosystem.

These applications signal a broader trend. Tech and consumer companies see banking as infrastructure, not a separate industry. Why partner with banks when you can become one?

For regulators, the challenge becomes managing this influx without compromising safety. Banks fail. Always have, always will. The question is whether new entrants understand banking risks or just see easy money in a loosely regulated environment.

PayPal’s decades of financial services experience suggests they grasp the complexities. Their $30 billion lending track record proves they can assess and manage risk. But regulatory approval is just step one. Actually operating a bank successfully requires sustained competence and discipline.

The next few years will reveal whether Trump-era banking deregulation creates genuine innovation or sets up future crises. PayPal’s application is just one data point. But it’s a significant one, given their scale and existing customer base.

Watch what happens when these approvals convert to actual operating banks. That’s when we’ll know if loosening rules was genius or reckless.